73 social media sites and 12 months of change: A social media taxonomy – update 2013

Each October, I look at the state of play in the social media scene. Which sites are successful? Why? Who are the players? What adds value and what is just noise? This is for my own curiosity (some may say compulsion), I invite you to engage with the research as it adds value to your world. Welcome to year three of my attempt to make sense of the dynamic social media space.

What I said in 2011: Creating parameters and the “why”

First, taxonomies have been done before. Many are prettier, and I do not address tools used with social media. However, as I have mentioned before: if I have not done it, then it has not been done.

Second, I acknowledge those who say ranking by Alexa is a waste of time and those who use the information are morons. Some say there is some relevancy when comparing similar high-traffic sites. I say more about this in the disclaimer at the bottom of this post.

Third, the time spent formatting my research for public consumption could have been spent on something more meaningful. As it is, I struggle with an internal paradox of supporting the propagation of a medium I hold in critical view. Social media channels have the potential to drive community, but can be perverted by two factors: 1) inappropriate expression of the commercial mandate that can manipulate intent; and 2) the expression of personal character deficiencies allowed through anonymity.

However, one should be knowledgeable about fields in which they both promote and of which they are critical and hope to improve. My post allows me to capture my thoughts for future reference and may be of interest to those not immersed in the field.

What I said in 2012: Deciding what to include and exclude

2012 saw some high tech IPOs such as Facebook and Yelp, with most dropping value soon after launch. There is debate as to whether the social bubble has burst and whether Facebook is holding the pin. Part of the desire of doing this post year on year is to assess the accuracy of pundits and hold myself accountable for my own opinions and observations.

I do not include in my analysis hosted solutions such as Jive Software, which purports to be a social media platform for business although there are criticisms and they posted a US$55.8 million loss on US$77.3 million revenue. The business social space will be interesting to watch, with Microsoft coming to the table with a purchase of Yammer, which Jive argues is a criticism of Microsoft’s positioning of SharePoint’s social capabilities.

Paid or install-only solutions such as Typepad or Movable Type that can act as social platforms are also not included, although I did include social CMS platform Ning from back in 2011 and I acknowledge WordPress can be used as a stand-alone CMS solution.

I also do not include sites that have a primary engagement through distributed channels like Facebook. These include troubled social gaming provider Zynga or music subscription services like Spotify or rdio for music.

With the continued growth of mobile, I will start to include solutions that have an app-only expression such as Path and Kilroy even though they will throw off my alexa rankings model. Smartphone growth rate is decreasing, tablet growth is increasing, and laptop and desktop sales decrease. That said, I question whether the time is right yet for an app-only interface to compete with solutions that are across all devices.

I am adding non-English sites on a case by case basis based on my limited exposure and understanding. China’s social media landscape and in particular their Facebook counterparts is a whole other world.

Finally, this does not acknowledge the contingent of open-source distributed social networks such as Diaspora and buddycloud. These alternatives are healthy in a competitive market and can produce innovation. For the short term, it is a movement that is likely to be noted only by the more technically-minded.

2013: Looking at macro trends

Big social media players are getting bigger. Low barriers remain in a space where anyone can learn code and create a software platform. Success is defined not just be a new idea, but by access to networks, like financial and social networks.

Entrepreneurs who found success in the land grab of the past leverage those networks for new projects. We see the Last.fm founders launch into Lumi, a new information aggregation and presentation model. The founder of Newsvine has secured $1 million for his new yet-undefined venture, BeLeave. Twitter and Blogger entrepreneur Evan Williams redefines content with his new platform Medium. The 33-year old behind mobile app Path had a history in Apple and Facebook. The recent Twitter IPO created millionaires of 1,600 employees, adding to the ranks of what can be referred to as the “Twitter Mafia” of technologists ready to start something new.

We see the start-ups of yesteryear become the institutions of today. The rate of change is prompting start-up cultures inside commercial institutions, in academic institutions, and through the creation of whole new disruptive institutions.

It is apparent that the online start-up game is a long-haul. Jive Software I mentioned last year reported in November a loss of $53.1 million and an accumulated deficit of $205.2 million, even as they paid $6.5 million for cloud-based analytics platform Clara and fair value purchase of $7.3 million for StreamOnce which connects third-party information streams. As they declare: We have a history of cumulative losses and we do not expect to be profitable for the foreseeable future. This may be why new entrant in the business social space Zepplin did a pivot to award winning executive dashboard Databox and is now based out of PayPal’s StartTank.

The space is not for the faint of heart. The rewards are huge, the risks major, and the impacts on our social structure significant.

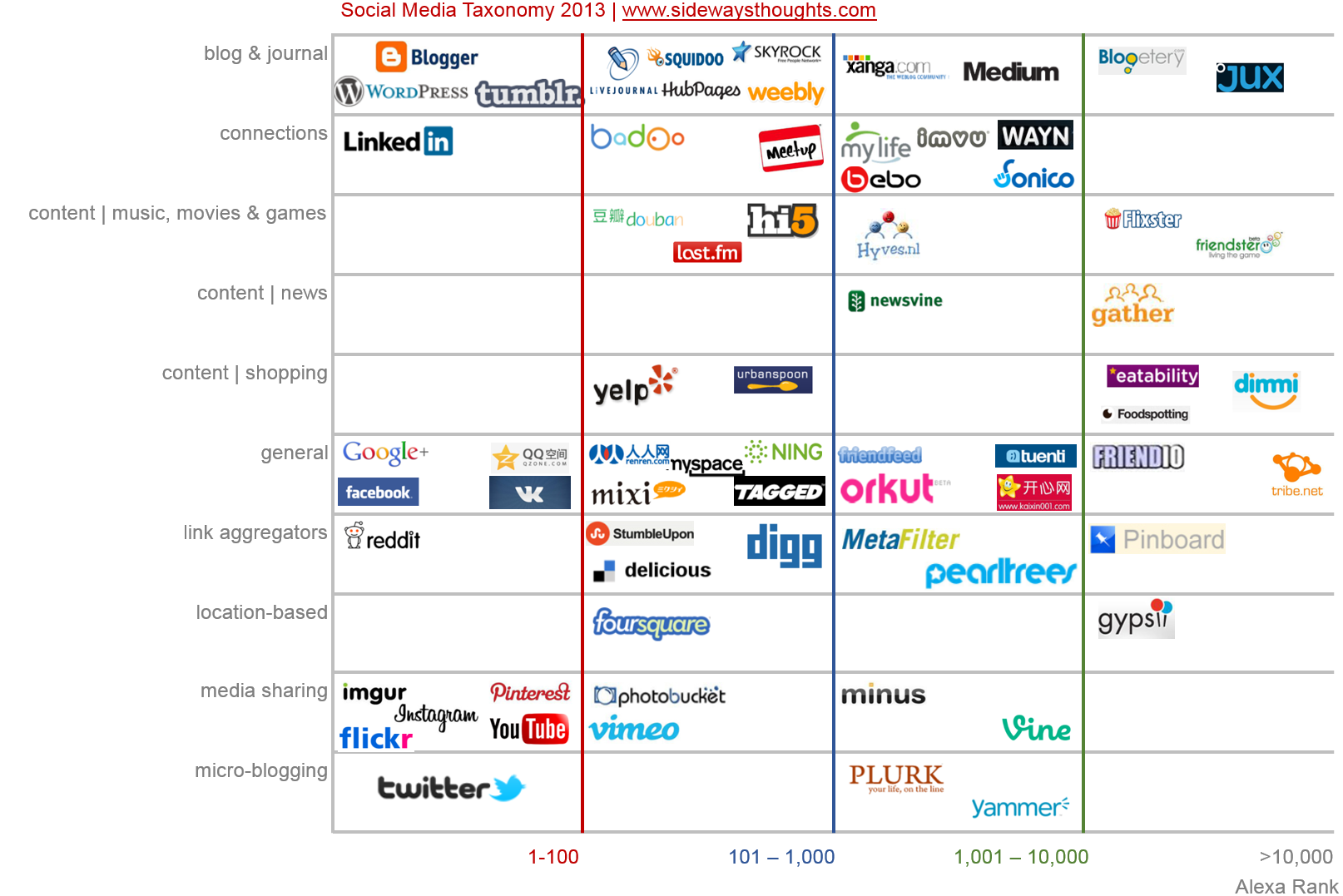

The sites and approach

The sites are below. If you are a member of any of these, please feel free to find, friend, fan, follow, or whatever other fun “f” word applies to the respected site. If there is some glaring omission or correction needed, let me know.

For each category, I copy over my thoughts from the previous years to reflect on what was top of mind at the time and keep me accountable for my opinions.

Blogging / Journal |

|

The focus for the Blogging / Journal category is on the user’s posts, where the intention is that the posts are done on a regular basis (which excludes website static content) and is typically of a greater length (which tends to exclude micro-posts).

2011Blogger is a Google social media success, rare for the organisation. The WordPress figures do not account for sites that host their own, like this one you are reading. Tumblr touts being easy to use. LiveJournal and Xanga, I am still coming up to speed with. 2012I gave Tumblr a try, for reasons I talk about here. I then stopped, as I discuss here. I also started a new Blogger blog here called the FIN Review review, but I find the search engine optimisation very poor compared to WordPress and I am unsure if my time commitments will let me keep the site going. I added Skyrock (strong in France), Blogetery (WordPress substitute that uses WordPress, bordering on irrelevant), Posterous Spaces (Twitter-owned version of Tumbler with features like Google Plus Circles) and Jux (quite cool space that is all about the imagery). Jux may have potential, signing up was a cool experience and makes me want to go back… or it may be just like a WordPress theme. 2013The big three blogging platforms of Blogger, WordPress and Tumblr are still big. It will be interesting to see how Google’s Blogger integrates with Google Plus, WordPress now powers around 19 percent of the Internet, and Yahoo paid $1.1 billion in cash for Tumblr which is now expanding into Asia while losing key staff. Posterous was a casualty of 2013 after being acquired by Twitter. Jux said they were closing their doors and I even wrote a nice obituary here, but it looks like someone put their money behind the meaning to keep the site alive. Other platforms stay alive due to cultural relevance, such as LiveJournal where over half the traffic hails from Russia and Skyrock which is strong in France. Xanga struggles to find relevancy and relaunched in September announcing Xanga 2.0 (do we still call web things 2.0?). A new noteworthy addition is Medium, started by founders of Blogger and Twitter. It promotes a simple interface and an interesting feature to add comments against paragraphs. As of this writing, there were around 84 categories containing 41,391 posts on the site. Hunter Walk writes here how it represents the new magazine content. The platform appears to be thriving due to simply being the cool place to be at the moment. It will be interesting to see if it is an evolution in social media or if it is a platform made popular by association. I also added Weebly (a build-your-own-site platform), Squidoo (started by digital celebrity Seth Godin, uses “lenses” instead of categories, focuses on link revenue), and Hubpages (also primary focus on link revenue). These sites focus on blogging for revenue, as compared to creating a place for self expression. A first hand comparison of the revenue potential between Bubblews, Squidoo, HubPages, and Zazzle can be found here. Much like struggling Farmville game maker Zynga’s reliance on Facebook, these sites are highly dependent on search engine traffic to justify their existence. This means it can be risky to build a career based solely on blogging revenue due to changes to search engine algorithms, as noted by Hubpages CEO in reference to Google’s change their Panda update. Sites like Hubpages also struggle with people gaming the system, diluting the quality of content and justifying Medium’s position of placing value on user-rated content. Case in point, I was presented with a strong message when I signed up to Squidoo about not gaming the system: “if you’ve actively swapped ratings, added countless affiliate links and focused on the short-term, we need you to take action now. It’s simple: go through your lenses, make them personal, delete extraneous affiliate links and ugly buttons. Make them the sort of thing you’d like to see, not the product of gaming the system and industrialized linkbaiting.“ |

|

|

Blogger WikipediaXang Alexa rank 2011: 6 Alexa rank 2012: 47 Alexa rank 2013: 43 My profile |

|

Tumblr Wikipedia Alexa rank 2011: 46 Alexa rank 2012: 36 Alexa rank 2013: 24 My profile |

| WordPress Wikipedia Alexa rank 2011: 77 Alexa rank 2012: 97 Alexa rank 2013: 68 My profile |

|

|

Livejournal Wikipedia Alexa rank 2011: 89 Alexa rank 2012: 118 Alexa rank 2013: 129 My profile |

| Xanga Wikipedia Alexa rank 2011: 2794 Alexa rank 2012: 4159 Alexa rank 2013: 8141 |

|

| Skyrock Wikipedia Alexa rank 2012: 815 Alexa rank 2013: 878 My profile |

|

| Blogetery Alexa rank 2012: 10,381 Alexa rank 2013: 43,244 My profile |

|

| Weebly Wikipedia Alexa rank 2013: 246 My profile |

|

|

Medium Wikipedia Alexa rank 2013: 4,623 My profile |

| Squidoo Wikipedia Alexa rank 2013: 550 |

|

| Hubpages Wikipedia Alexa rank 2013: 541 |

|

|

Jux Wikipedia Alexa rank 2012: 68,417 Alexa rank 2013: 41,171 My profile |

Connections |

|

The focus is on making a connection between two or more people, as distinct from a site where the focus is on the individual expressing themselves and having the connection be a secondary function. I exclude sites where the connection is specific to romantic relationships, aka “dating sites”. Yes, the line is blurry.

2011LinkedIn is like professional dating, with job offers in lieu of marriage proposals. Meetup captures event management with an underlying premise of meeting for a purpose. IMVU is a quirky 3D chat world, but I would not trust sending my kid in there until she is 30. Being able to purchase intimate positions was kind of odd. I have not spent a great of time on the other sites, although my inbox gets regular love from people wanting to meet me despite my status of “taken” and “not interested”. 2012LinkedIn is the only site I have visited in the past 12 months. Twitter recently pulled their feed to LinkedIn, which cleaned up LinkedIn’s news feed and only strengthened LinkedIn’s position in the market. I took down my profile from a few sites because they would not let me have a profile without saying I was looking to meet someone else, placing me in an awkward position with my wife. Many sites are increasingly reliant on advertising dollars, as evident by WAYN which makes my profile look like it is on ebookers.com. I added Hungarian meeting site OpenMeetup which is invite-only and poorly executed OpenCirclez, both of which I question as to whether we will see next year. 2013LinkedIn has gone from strength to strength. The platform’s value is about five times its 2011 IPO of $45, it continues to launch new products like Sponsored Updates and University pages, and dropped its minimum age to 14 years to focus on the incoming pool of talent. Its revenue from the Talent Solutions recruitment function has grown 100% in the past year and brings in 54% of its revenue ($523 million, or 2% of the available $27 billion market). I keep Badoo on the list, but it really is more of a dating site disguised as a social network. Netlog is off the list, having been acquired by the parent company of dating site Twoo.com late 2012 and rolled into that site. Bebo, which was purchased in 2008 by AOL for $850 million when it had 40 million users, was bought back by the original founder for $1 million and put in a temporary hiatus as explained in this video. Meetup has established itself as the connecting platform of choice, with last year’s entrants OpenMeetup and OpenCirclez no longer around. Virtual world IMVU is in its ninth year and going strong. By the numbers, it has 11 million registered users, over 3.3 million monthly active participants, earns $55 million in revenue, and the core audience is 65% female, 50% in the US, and the average age is 25. WAYN has established itself as specialising in the social travel scene, reaching 21 million users and creating key partnerships with players n the travel industry. |

|

| LinkedIn Wikipedia Alexa rank 2011: 12 Alexa rank 2012: 12 My profile |

|

| Badoo Wikipedia Alexa rank 2011: 104 Alexa rank 2012: 133 Alexa rank 2013: 164 |

|

|

Meetup Wikipedia Alexa rank 2011: 461 Alexa rank 2011: 363 Alexa rank 2012: 325 My profile |

|

MyLife Wikipedia Alexa rank 2011: 1138 Alexa rank 2012: 2047 Alexa rank 2013: 3063 |

| WAYN Wikipedia Alexa rank 2011: 1401 Alexa rank 2012: 1645 Alexa rank 2013: 3345 My profile |

|

| Sonico Wikipedia Alexa rank 2011: 1700 Alexa rank 2011: 2755 Alexa rank 2013: 5405 My profile |

|

| IMVU Wikipedia Alexa rank 2011: 2319 Alexa rank 2011: 3224 Alexa rank 2013: 5443 |

|

|

Bebo Wikipedia Alexa rank 2011: 2662 Alexa rank 2012: 4463 Alexa rank 2013: 8327 |

Content-specific |

|

A site where a type of content is provided for the purpose of soliciting interaction, as compared to a site where the content is the focus and the interaction is secondary.

2011A few non-English sites in here to challenge those that think social media is a western culture phenomenon. Interesting Ted talk on the scale of China’s youth engagement here. Other sites revolve around games, movies, shopping, and news. If you have a common interest, you can have community. 2012Sites that deliver content with a social expression are at risk if larger entities like Facebook or Google deliver that same content. Shopping site Multiply shut down its social networking service based on sites like Facebook better serving those needs. Yelp stocks remain strong, but will always look over its shoulder at the likes of Google+ Local or Foursquare. Given Yelp’s popularity, expect to see similar review sites. Yelp was not offered in Australia this time last year, and it seems to have issue with letting me change my location from Seattle. Additions in 2012 are openMarkers, Urbanspoon and Foodspotting. Social and gaming has moved to almost exclusively gaming, with this year’s Friendster redesign, placing it in the same crowded market as game delivery channels occupied by the likes of Kongregate and Newgrounds. The next year will be interesting to see what remains in this list. 2013I removed OpenMarkers; their Twitter and Facebook links have been quiet since January and the site has moved to a free hosting service. Now in its ninth year, publicly listed Yelp posted a loss of $2.33 million, revenue increased 80% from 2012, cumulative reviews grew 42 percent to over 47.3 million, average unique visitors grew 41 percent and local business accounts grew 61 percent to 57,000. CEO Jeremy Stoppelman shares a mobile-focus with many social platforms, given that 62% of Yelp searches are done on mobile devices. Review sites such as Yelp have significant ability to disrupt business, with online reviews making or breaking a business, to the point of being able to be used as blackmail as told here. Another step for sites like Yelp is to close the transaction by offering reservation services, and I imagine that introducing basic online ordering is not too far away. Yelp competitor OpenTable seated 38.5 million diners in Q3 2013, an increase of 30 percent with 41 percent of bookings made through mobile devices. OpenTable purchased UrbanSpoon’s reservation system in July as well as acquired Foodspotting for $10 million. Yelp acquired reservation application SeatMe in the same month for $12.7 million. I came across this comparison of traffic from food review sites, which includes Optus-owned Eatability which recently relaunched a mobile app and online reservation, and review system Dimmi, which is backed by Telstra and Villiage Roadshow and has deals with tripAdviser. Dutch networking site Hyves has announced an exclusive focus on games as of December 2013. which may mean I pull them from the list if they end up looking more like Kongregate or Newgrounds that focus more on games than social. Chinese site Douban appears to continue in strength. After shutting down the social aspect in 2012, shopping site Multiply closed up shop altogether and has been removed from the list. Hi5 was acquired by Tagged in 2011 but still maintains its own identity. Friendster continues an apparent decline as does Flixter who now appears to struggle with irrelevance in light of sites like Hulu and Netflix that offer full media viewing service rather than just talking about it. CBS-owned social radio service Last.fm redesigned their Microsoft’s Xbox 360 interface and made modifications to overseas radio services as it competes and integrates with other services. The real value in the service as with all content-specific social sites is in tracking the behaviour of users. This is known by the original last.fm founders, who after getting bought out in 2007 for $280 million are now launching Lumi to help people better find things online based on browsing history. News site Gather appears to be slipping in relevance, while NBC’s NewsVine seems to stay strong albeit with some criticism over a redesign earlier this year. Newsvine co-founder Nick Hanauer recently raised $1 million for a new start-up called BeLeave. |

|

| Douban Wikipedia Alexa rank 2011: 113 Alexa rank 2012: 126 Alexa rank 2013: 226 |

|

|

Yelp Wikipedia Alexa rank 2011: 171 Alexa rank 2012: 229 Alexa rank 2013: 134 My profile |

|

Urbanspoon Wikipedia Alexa rank 2012: 1917 Alexa rank 2013: 1739 My profile |

| Eatability Alexa rank 2013: 64,047 |

|

|

Dimmi Alexa rank 2013: 112,867 |

| Foodspotting Alexa rank 2012: 19,436 Alexa rank 2013: 11,048 My profile |

|

|

Hi5 Wikipedia Alexa rank 2011: 567 Alexa rank 2012: 622 Alexa rank 2013: 998 |

| Last.fm Wikipedia Alexa rank 2011: 589 Alexa rank 2012: 929 Alexa rank 2012: 959 My profile |

|

|

Hyves.nl Wikipedia Alexa rank 2011: 765 Alexa rank 2012: 3653 Alexa rank 2013: 8425 |

|

Gather Wikipedia Alexa rank 2011: 2176 Alexa rank 2012: 3233 Alexa rank 2013: 10,052 My profile |

| Newsvine Wikipedia Alexa rank 2011: 2392 Alexa rank 2012: 3700 Alexa rank 2013: 3609 My profile |

|

|

Friendster Wikipedia Alexa rank 2011: 3934 Alexa rank 2012: 15,368 Alexa rank 2013: 18,969 My profile |

| Flixter Wikipedia Alexa rank 2011: 628 Alexa rank 2012: 8259 Alexa rank 2013: 14,232 |

|

General |

|

A catch-all for sites that allow personal expression without a stated focus on meeting others or a type of content or functionality, although these are provided.

2011Facebook is thirty-six times the population of Australia. If it ever falls, it will make a noise. Google Plus, I am not seeing the value. The hype around circles was just noise, as I do not see enough people posting to warrant filtering. At least MySpace seems to be about the music, giving it some sort of distinction. Plurk has an interesting timeline, although interesting does not translate into useful. Orkut is another Google platform, which makes me think that along with Google Wave and Google Buzz they just keep trying until something sticks. Ning is an odd man out as a type of Content Management System for social media. 2012There are now over a billion people on Facebook (Earth’s population is 6.9 billion if you need a point of reference). Words like “monopoly” are being used as Facebook starts have people pay to “promote” posts that used to be seen for free. Google Plus is being called a ghost town due to a lack of demand. Myspace is attempting to reinvent itself under new owner Justin Timberlake and I expect to move it to the content area next year if the new design is launched. Google’s Orkut is now linked to Google Plus, to where it asked me to link the accounts (e.g., “upgrade”) when I checked out my profile this year. Spain-based Tuenti appears to be opening up to the wider market, although I could not get passed their SMS-based registration system. Russian-based VK also had SMS confirmation, which interrupts the log in process. I still think Plurk is interesting. Interesting does not equal useful. Friendio launched out of alpha in February. It’s like Facebook, except without your friends. I also added Russian social site VK and Chinese sites QZone and Renren. 2013Facebook is now in year two of opening itself to the rigour of a publically-listed company and it continues to drive innovation to support its position. Its Messenger app is branded as a stand-alone product, its focus on mobile resulted in mobile ad revenue increasing 41 percent from the previous quarter to represent over 49 percent of total ad revenue, and it is rumoured to be chatting acquisition with BlackBerry. With over a billion active users per month seeing one ad per 20 posts, it may be one of the few platforms that can exist solely on an ad revenue model. These numbers make the platform seem permanent and reports of teens moving away from the platform seem almost irrelevant. The ubiquitous nature of the platform makes headlines of even slight changes in “like” buttons. The platforms impact on our social structure is significant, from wide-spread employment privacy settings to its role in cyber-bullying and suicides. Spain-based Tuenti is also focusing on mobile, not surprising given Spanish telecommunications provider Telefonica this year acquired all remaining shares in the social platform. Like Facebook, Tuenti is seeing a future in global messaging as it launches its Social Messenger application in twelve languages which had 150,000 customers in its first year as of June 2013. Google Plus exists because of the “Google” part. Publishers do not even consider the platform as a traffic source, representing around 0.04 percent of traffic referrals compared to Facebook’s 10.4 percent. Google’s approach appears to be blunt force trauma, forcing anyone using Gmail or YouTube to have an account. The jury is still out on the role MySpace will play moving forward, as it recently announced laying off five percent of its staff. Google’s Orkut remains big in Brazil and some say is still around simply because closing it would reflect poorly on Google Plus based on comparisons to other social media non-events by the company including Wave, Jaiku, and Buzz. FriendFeed feels as awkward as Orkut, in that it was acquired by Facebook in 2009 and now just sits in seemingly obscurity. The process gave credibility to the original Stanford grad founders, however, who are now looking at new start-up Quip which offers word processing on mobile devices. Social platform Tagged remains relevant to some, releasing their Sidewalk app earlier this year. I like the frankness with which Tagged CEO states his awareness of what the platform is, and is not: “For three years we competed to become the world’s social network. We realized by the end of 2007 that there was going to be one winner and it wasn’t going to be us. So we made the difficult decision to pivot into social discovery, which is a fancy way of saying ‘meeting new people.” Social platform Ning redefined itself again with Ning 3.0, offering a paid publishing service that some say may be a challenge in a crowded market. Tribe.net may not be long for this world as indicated by the Tribe.net Purists tribe set up under religions and beliefs which has a total of two members. It may be a race to the end with Friendio, which I can find nothing on apart from a February 2012 press release that says the platform is booming. Social mobile application Path was adding 1 million new users per week in April and declared an ad-free business model in September when they were around 10 million active users. In October, the 50-person company, which has raised $41.2 million since starting in 2010, axed 20 percent of its workforce. The platform currently says it has 20 million registered users and charges $14.99 for premium privacy features.

|

|

|

Facebook Wikipedia Alexa rank 2011: 2 Alexa rank 2012: 1 Alexa rank 2013: 2 My profile |

| MySpace Wikipedia Alexa rank 2011: 103 Alexa rank 2012: 192 Alexa rank 2013: 753 My profile |

|

| Orkut Wikipedia Alexa rank 2011: 126 Alexa rank 2012: 578 Alexa rank 2013: 2189 My profile |

|

| Mixi Wikipedia Alexa rank 2011: 155 Alexa rank 2012: 376 Alexa rank 2013: 944 |

|

|

Kaixen001 Wikipedia Alexa rank 2011: 201 Alexa rank 2012: 265 Alexa rank 2013: 1945 |

|

Tagged Wikipedia Alexa rank 2011: 276 Alexa rank 2012: 241 Alexa rank 2013: 381 |

| Ning Wikipedia Alexa rank 2011: 299 Alexa rank 2012: 464 Alexa rank 2013: 439 |

|

| Tuenti Wikipedia Alexa rank 2011: 767 Alexa rank 2012: 1206 Alexa rank 2013: 3391 |

|

| Friendfeed Wikipedia Alexa rank 2011: 1116 Alexa rank 2012: 1558 Alexa rank 2013: 1505 My profile |

|

|

Tribe Wikipedia Alexa rank 2011: 7120 Alexa rank 2011: 6591 Alexa rank 2012: 11,293 My profile |

| Google Plus Wikipedia Alexa rank: unknown – sub domains not counted My profile |

|

|

Path App only |

| Friendio Alexa rank 2012: 1,076,983 Alexa rank 2013: 7,474,773 My profile |

|

|

VK Wikipedia Alexa rank 2012: 29 Alexa rank 2013: 22 My profile |

|

QZone Wikipedia Alexa rank 2012: 9 Alexa rank 2013: 7? (qzone appears to be a subdomain of parent news site qq.com, much like Google plus is to Google) |

| Renren Wikipedia Alexa rank 2011: 130 Alexa rank 2012: 155 Alexa rank 2013: 157 |

|

Link Aggregators |

|

Sites that promote interaction around a user’s collection of links. Places you can save and share links.

2011I don’t have the time myself to surf someone else’s distractions, but I hear others find these of value. 2012I tend to rely on Twitter and my studio word of mouth to keep up on Internet happenings. That said, link aggregators have come a long way in the past 12 months. Stumbleupon has gone through a couple of redesigns here and here as have Delicious and the Digg. Reddit by comparison has maintained a simplistic design. The Digg relaunch now forces Twitter or Facebook log in, blowing away my previous profile and any notion of a profile page. Pinboard has been around a few years, but the one-time entrance fee is a barrier to me. There are sites like Zootool that I leave off the list due to a perceived focus on bookmarking over social. Grazely is invite only, and may get to the list next year. Pistashio is Twitter-only log in, so will need to wait to next year to see if it is around to make the list. Link shorteners like bit.ly are adding social elements, but also not on the list. 2013StumbleUpon restructured in January and let go 30% of its then 110 staff, closed down its su.pr URL shortener in July, had a shift in Product leadership in August, purchased video-curation start-up 5by in September, and joins the mobile movement with lists now available on iPhones and iPads. All these activities contribute to a report that the company is now profitable, growing revenue up 33 percent with its 30 million registered users and 100,000 advertisers. Reddit continues in popularity, with recent Ask Me Anything (AMAs) participants including Yelp CEO, previous Australian Premier Kevin Rudd, and Ann Coulter in what has been described as the worst AMA ever. It is estimated that six percent of online adults are Reddit users and earlier this year the site started accepting Bitcoin for its subscription services. Here are some tips if you want to be in the six percent and some challenges the platform is facing with content bans. Digg, once valued at more than $160 million, sold for $500,000 in 2012 to BetaWorks who rolled it into news aggregator site News.me and which also owns brands such as bit.ly, InstaPaper, and SocialFlow. A great backstory on Wired and a different perspective on Inc. talk about the transition and how the team worked to address the gap left by Google closing Google Reader. The site continues to try to innovate with the recent release of Digg video as a response to reddit.tv, even as some continue to talk about the death of Digg. The Delicious platform, bought by Yahoo in 2005 and later sold in 2011, showed some signs of life in 2013. The site received a redesign in January and added some social features in March but it may not be enough to maintain relevance. Metafilter has been around since 1999. That’s forever. In this interview, CEO Matt Haughey doesn’t “know exactly what keeps the site around or keeps people coming back” and is kind of terrified of the pace of change on th eInternet. Yeah, me three. I added French startup Pearltrees to the list. I don’t take the time to capture my links, but I love the mind mapping interface. The site launched in December 2010 and has two million active users and collects over 50,000 links every day. The company has raised around $11.5 million and charges for premium services that offer increased privacy. There’s a great interview with the CEO who shares 9 lessons, including the fact that they didn’t pivot. Grazely and Pistashio did not make it through the year. A moment of silence please… OK, that’s enough. |

|

| Stumbleupon Wikipedia Alexa rank 2011: 105 Alexa rank 2012: 151 Alexa rank 2013: 150 My profile |

|

|

Reddit Wikipedia Alexa rank 2011: 115 Alexa rank 2012: 136 Alexa rank 2013: 85 My profile |

|

Digg Wikipedia Alexa rank 2011: 169 Alexa rank 2012: 493 Alexa rank 2013: 470 |

| Delicious Wikipedia Alexa rank 2011: 305 Alexa rank 2012: 539 Alexa rank 2013: 856 My profile |

|

| Metafilter Wikipedia Alexa rank 2011: 1540 Alexa rank 2012: 2214 Alexa rank 2013: 3358 |

|

| Pearltrees Wikipedia Alexa rank 2013: 6231 My Profile |

|

| Pinboard Wikipedia Alexa rank 2012: 16,483 Alexa rank 2013: 21,439 |

|

Location-based |

|

Sites that focus on checking into locations, as compared to sites that have check-ins only as a function.

2011Foursquare stands out as a system focused on check-ins. There may be others. You can read my full thoughts here. 2012Foursquare still owns the space. Gowalla shut down this year after being acquired by Facebook before I realised I forgot to add them. Whrrl was acquired by Groupon and shut down. Brightkite which is said to have started checkins also closed down. Buzzd closed in 2011 and became marketing tool local-response. Pure location-based without a revenue model is a bit of a challenge. 2013Foursquare is still the dominant player solely focused on location. Rumoured to be in talks of acquisition, it recently launched the ability for businesses to server their own ads. The founder says the platform is never done, even as others call for the site to go back to its roots. The biggest threat to the platform could be getting cut off from traffic from the likes of Facebook and Google. Facebook-owned Instagram’s 150 million users drive a lot of traffic to the smaller 40 million user Foursquare. If Facebook and Google decide they want to cut the connection to focus on check-in features on their own platforms, there could be trouble in Foursquare’s world. |

|

| Foursquare Wikipedia Alexa rank 2011: 602 Alexa rank 2012: 867 Alexa rank 2013: 482 My profile |

|

|

Kilroy Mobile-only |

|

Gypsii Alexa rank 2012: 1,281,818 Alexa rank 2012: 3,729,171 |

Media-sharing |

|

Sites where the interaction is around user-generated non-text media, such as movies or images.Two words: Free content hosting.

2011YouTube needed a big player like Google behind it. I know I am missing some sites here. 2012Pinterest was the big news since the last update, although it was already big by last October. Instagram was also big news, in particularly Facebook’s $1 billion acquisition of the product. A full comparison of video hosting services is better done elsewhere. A few other image sharing sites have also been added to the list. 2013Google’s YouTube has transformed media. The platform is in a position to take additional TV advertising dollars as Google considers working with Nielson for improved online ad measurement. US online video advertising is expected to increase 43 per cent to over $A4.4 billion this year, as compared to a TV ad spend increase of 2.8 per cent to $66.3 billion. YouTube is estimated to account for a third of the total US video market. The impact is felt in the music industry as well, with this year seeing the first ever YouTube music video awards. Google is taking advantage of the size of the opportunity, recently forcing people who want to comment on videos to have a Google Plus account, resulting in a backlash and a petition with over 112,000 signatures. Other’s ride on the back of the volumes, such as a cake maker who made $17,000 in an hour after posting a video of the making of a spider-man cake. On a Google-related side note, Google-owned Picasa is redirecting to Google Plus. Vimeo continues to differentiate from YouTube, focusing on quality of content. This year the platform partnered with the Toronto Film Festival for exclusive access and supported the industry with creative paywalls for on-demand content. Even as it plays well with the movie industry, the debate continues over whether the uploader or the platform is responsible for copyright infringement. Yahoo’s Flickr got a face lift and some additional free storage space in May, even as some say Yahoo killed Flickr and killed the Internet. Yahoo continues to invest in the platform, acquiring facial recognition software LookFlow even as rival Photobucket overtakes with 26 million users. In keeping with trends in other platforms, Flickr’s original founders have gone off to now start something to manage the noise of the Internet they helped to create, a communication management platform called Slack. Photo-sharing site Imjur experienced 60 per cent growth and reached over 100 million unique visitors per month. Social scrapbooking site Pinterest raised $225 million and is valued at $3.8 billion, and is yet to generate revenue with its 150 employees. Not all platforms can be as lucky. Photo sharing site DailyBooth, which raised $7 million in 2011, was bought in a talent acquisition in July 2012 and was shut down end of 2012. The social image space is heating up. Instagram filters have become pervasive and cliché. Some say Instagram should have held out before selling to Facebook, even as SnapChat turned down Facebook’s $3 billion offer. Social platform Minus also thinks we might want to chat with strangers around us who also take photos. Twitter’s Vine makes everyone a celebrity for six seconds even is the platforms own celebrity star competes with Instagram. |

|

|

YouTube Wikipedia Alexa rank 2011: 3 Alexa rank 2012: 3 Alexa rank 2013: 3 My profile |

| Flickr Wikipedia Alexa rank 2011: 33 Alexa rank 2012: 58 Alexa rank 2013: 65 My profile |

|

|

Vimeo Wikipedia Alexa rank 2012: 128 Alexa rank 2013: 104 |

|

Picasa Wikipedia |

| Minus Alexa rank 2012: 1527 Alexa rank 2013: 1376 My profile |

|

| Snapchat Mobile app |

|

|

Vine Alexa rank 2013: 2072 |

|

imgur Wikipedia Alexa rank 2012: 96 Alexa rank 2013: 62 |

| photobucket Wikipedia Alexa rank 2012: 171 Alexa rank 2013: 202 |

|

| Pinterest Wikipedia Alexa rank 2012: 38 Alexa rank 2013: 27 My profile |

|

|

Instagram Wikipedia Alexa rank 2012: 58 Alexa rank 2013: 39 My profile (via followgram) |

Micro-blogging |

|

Sites that focus on short posts, usually limited in character count. An example of a conversation turning into a one-way information push (guilty as charged).

2011Seems only room for one big player, although others try to corner markets, such as Yammer for secure conversations. 2012Twitter and LinkedIn parted ways this year, resulting in a more valuable LinkedIn new feed. Microsoft bought Yammer for alignment with its SharePoint service as it prepares for competition in the business social space with the likes of unprofitable Jive Software and new startup Zepplin. Qaiku called it quits this year even thought the service remains up at this time. Jaiku also closed it doors after acquisition by Google. There are questions as to whether identi.ca will be around next year. 2013The ink is still dry on Twitter’s IPO, which created millionaires of 1,600 employees who will now collectively pay $2.2 billion in taxes. The company s valued at $USD 23.96 billion, with a revenue of $534.5 million and losses of $64.6 million and 231.7 million users. Microsoft’s Yammer stays on the list, although it’s enterprise-only model should really have it in a space to its own even as some say it is killing enterprise social networking. Identi.ca stopped taking registrations. Plurk, which I moved from he general platforms category to micro-blogging, received a few million in funding and shifted its half-dozen developer engine to Taiwan in January. The CEO acknowledges it is now niche, but cites the higher per-user revenue spend in Asian markets as incentive for the move. I do not expect to hear much about it apart from a few curious developers poking it with a stick. |

|

| Twitter Wikipedia Alexa rank 2011: 9 Alexa rank 2012: 8 Alexa rank 2013: 10 My profile |

|

|

Plurk Wikipedia Alexa rank 2011: 1485 Alexa rank 2012: 2016 Alexa rank 2013: 1688 My profile |

| Yammer Wikipedia Alexa rank 2011: 3608 Alexa rank 2012: 3597 Alexa rank 2013: 3395 |

|

See you next year!

Disclaimer

- This is not every social media site. It is a random sample limited by my inclination and degree of obsessiveness. It may not include your favourite.

- Categories are subjective. Some sites can be in more than one category. This statement is categorically true.

- I used Alexa for relative ranking. Alexa gets stats from people who install Alexa’s toolbar. People say Alexa stats should not be used. I used Alexa for relative ranking of similar high-volume sites sites. Year on year comparisons can be influenced by changes in Alexa reporting population and methodology. Alexa was easier than using the site’s self-reported information. It might be better than guessing. Maybe.

- Alexa does not do sub-domains. Google Plus is a guess. See disclaimer 3.

- I looked at “social media” sites. I described these as “the product of the site is the sharing of personal details or content between two or more people who are not employed by the site”. Others use different descriptions. Some of those description use bad words.

- This information is based on a snapshot a week in October. Someone could build an application to dynamically rank and automatically categorise the sites at points in time. I am not that someone. If you are, send me a link.

Chad, A taxonomy deserving of recognition in an encyclopedia! Thank you for the incredible time and effort that would have gone into your post. I become the beneficiary of your distillation of the social media world.

Thanks John! I remember encyclopaedias. 😉

I am glad it added value.

Chad

I have seen a lot of these trends, especially on facebook. I recently got into the social media scene. I still feel like I am very young to it. It is exciting, and a little overwhelming to be part of something so big. I hope that this all keeps growing.